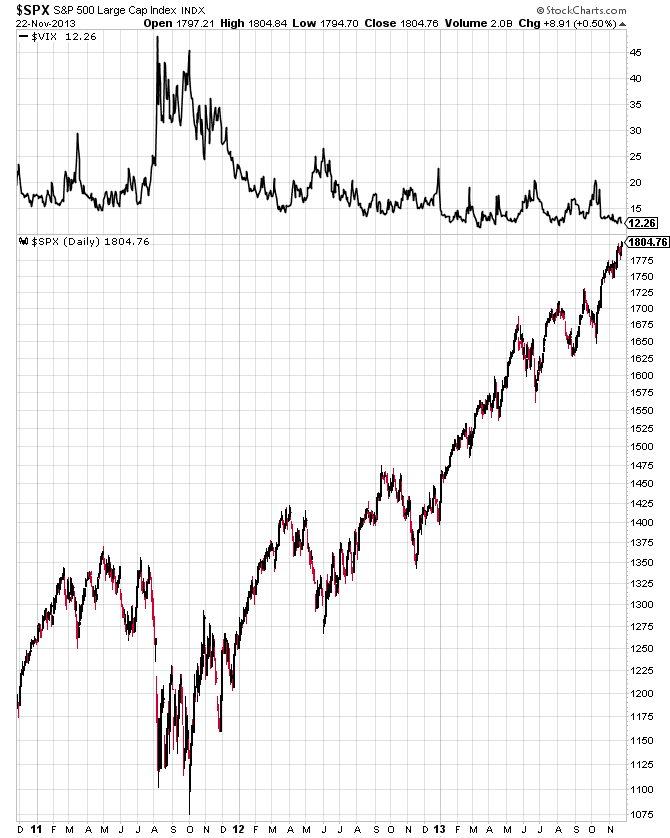

The S+P 500 and the Dow both closed the week at new all time highs. 1775 in the S+P 500 was key and it reacted very well. The next measured move upside target will now take the S+P 500 up to 1833 in the near term. In the long term I still maintain the market is getting quite overextended but another 3-4% upside is realistic.

The Volatility Index (VIX) remains very low, each time this year that the VIX hit 20 it became a reliable buy signal. A VIX below 20 generally suggests that pullbacks are short lived and shallow, more of the 4-5% variety, which is what we have seen.

The cumulative advance - decline line continues to show bearish divergences. This indicator has not moved much higher since the May highs meanwhile the S+P 500 is roughly 6% higher above it's May high. This means the advance has been occurring with fewer participants and is usually a precursor to a significant correction. However this is not a timing tool and these divergences to go on for awhile before it eventually settles itself out.

Three of the nine sectors within the S+P 500 also made new highs on the year. Those being Financials, Energy and Health Care.

Year to date relative strength in this market comes from Health Care, Discretionary, Industrials and Financials. Underperformance comes from Materials, Tech and Utilities.

The US Dollar continues to find support around the $79 level, it's year to date performance has been roughly flat. I am watching the lows at $79 going forward, as the last time we had a significant drop in the Dollar, it eventually put downward pressure on equities in 2011.

TLT (Bonds) found support again at $102 this week. Upside resistance now stands at $111.50 and $118 as denoted on the chart. Next support level below comes in around $96-$97. At that point it would about match the size of the drop during the 2009-2010 correction, which happened to be the biggest correction seen since TLT was introduced.

TLT would need to find support there or $87 will eventually get taken out afterwards.

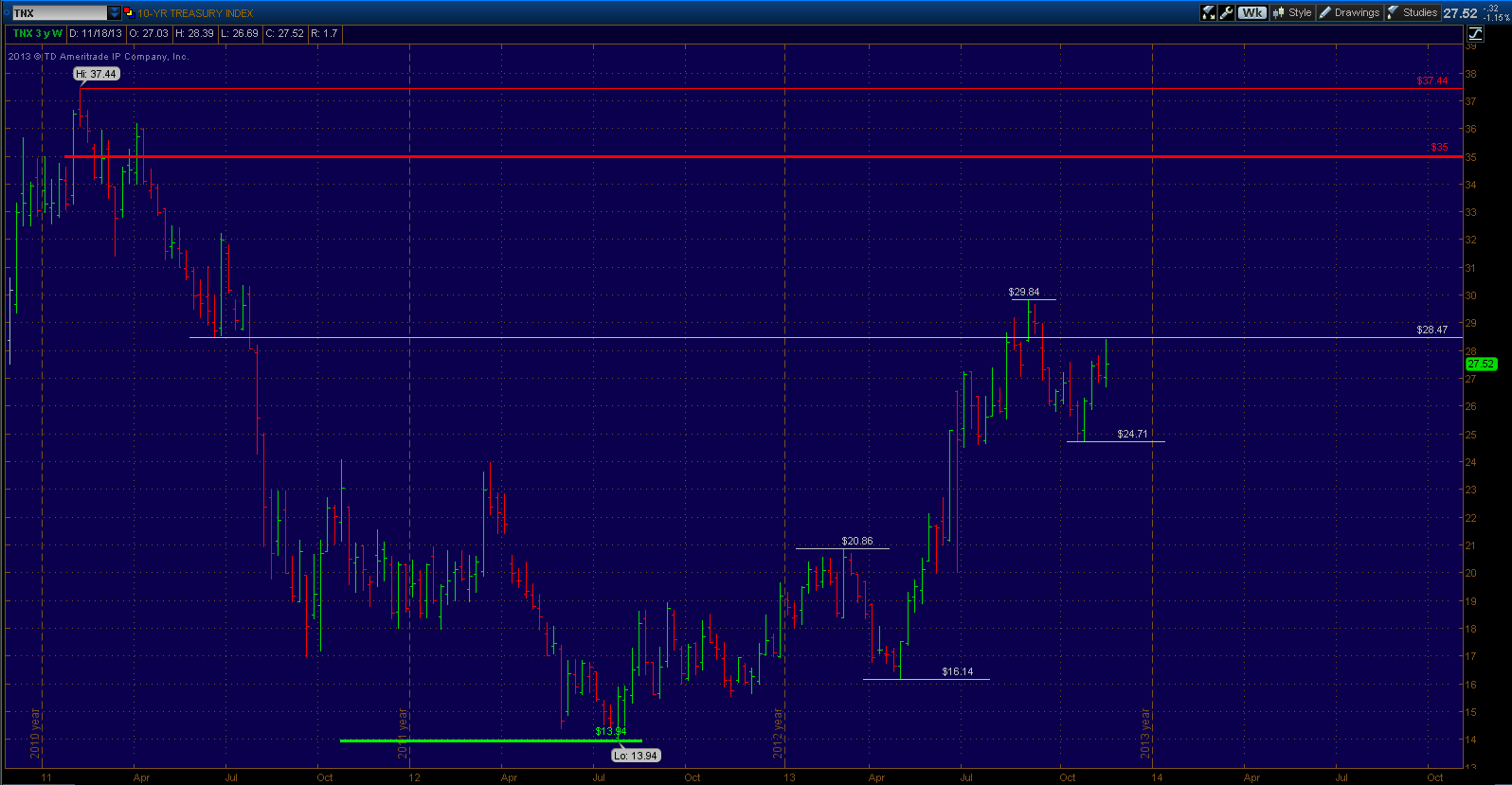

The yield on the ten year continues to hold above 2.5% after nearing the 3% area. It has completed a correction about the size of the one that took place early this year. The next upside comes in at 3.35% and downside support stands at 2.25%.

In conclusion, a look at year to date performance among asset classes. Obviously it's been a tremendous year for equities with Small Caps and Large Cap Tech leading the way with above 24% returns. Emerging markets are the laggards, with growth and "Taper" worries weighing heavily.